DEFINITION

The provenance and ownership history of an object/work from the moment of its creation to the present. This includes the means by which a work passed from one owner to the next; an identification of any public sales involving the work or the names of any agents who aided the transfer of ownership; and the names of any dealers who handled the work or included it in their inventories. If a work has been lost, stolen, or destroyed, or has otherwise vanished from public view, this fact should also be indicated here.

SUBCATEGORIES

- 23.1. Provenance Description

- 23.2. Transfer Mode / Method of Acquisition

- 23.3. Cost or Value

- 23.4. Legal Status

- 23.5. Owner/Agent

- 23.6. Ownership Place

- 23.7. Ownership Date

- 23.8. Owner’s Numbers

- 23.9. Owner’s Credit Line

- 23.10. Remarks

- 23.11. Citations

- Examples

GENERAL DISCUSSION

This category records what is known as provenance in the museum community. Provenance includes the history of all the people who have owned the work from its creation until the present, and the places where it has been located. The present custodian of the object/work is recorded in the category. Note that it is common to have lacunae in the provenance.

Provenance is recorded in order to trace the history of a work of art or architecture after its creation, and if possible to document legal title to a work at any particular time. The study of provenance in the museum community, particularly as it relates to the whereabouts of works from the Nazi era and World War II (1933-1945), is discussed in several publications.1

This category may also be used to record the history of the object/work’s posession, even if the person or corporate body in posession of the work was not the owner per se (e.g., the resident or occupant of a building).

Researchers are also interested in the provenance of works for a variety of other reasons. Provenance information is of great interest to scholars seeking to establish the whereabouts of a work at a given point or over time. Provenance establishes when a work was in a particular place, making it possible for researchers to discern whether it might have been seen by or have influenced others. A history of ownership also provides information about when possible interventions in the physical condition of a work, such as restoration, reformatting, remounting, changes, or additions, may have taken place. It provides insight into the activity of a collector or dealer, and makes it possible to establish patterns in collecting. Changing patterns in collecting illustrate the relative value of works of art, both as specific objects and as representatives of a style or period. This kind of information can enhance the understanding of the history of taste. A clear provenance can be used to establish the authorship of a work, or to link it to other related works. An illustrious provenance may enhance a work’s value or interest. An early or unbroken provenance may attest to its authenticity.

A record of the history of a work’s ownership is also useful in examining the formation of museum collections and in studying collection policies and de-accessioning practices. It may also illuminate how changes in laws, such as those governing taxes, influence the patronage of public collections.

The owner of a work on long-term loan to a public institution may be identified as either the lender or the custodian of the object, depending on local practice and/or the terms of the loan. Note that many private owners prefer not to be identified, or may specify only a limited designation, such as Private Collection, New York. This desire for privacy and security must be respected.

When works are in public collections, information on their provenance may be available from the current owner. It may also appear in up-to-date collection catalogs or catalogues raisonnés. When a work is in a private collection, this information may be limited or unavailable for security reasons. The history of ownership of a lost, stolen, or destroyed work may be based on published or unpublished sources, including newspapers, annotations in auction catalogs, letters, and other documents.

Provenance history rarely exists ready at hand and often must

be reconstructed from a variety of sources. Dates of ownership

are often extrapolated from other information, such as the

life dates of a particular owner, or the date on which a work

is recorded in another owner’s collection. Old inventories,

wills, correspondence, credit lines in exhibition catalogs,

auction or sale catalogs, newspaper accounts, oral testimony,

and dealers’ stockbooks may likewise provide clues.

Inscriptions or marks on the work itself, and labels attached

to it, may also provide information about previous owners of a

work. It may also be possible to identify the owner of a work

from evidence integral to the object itself, such as a

distinctive mat, mount, or numbering system. For example, the

coat of arms of Cardinal Albrecht of Brandenburg appears on

folio 1 of a prayerbook, so it is logical to assume that he is

the one who commissioned the work. Clues to the history of

ownership may also be found in published works, including

indexes to sales, such as Frits Lugt,

Répertoire des catalogs des ventes publiques…, and

those cited elsewhere in the description, such as exhibition

or permanent collection catalogs.2

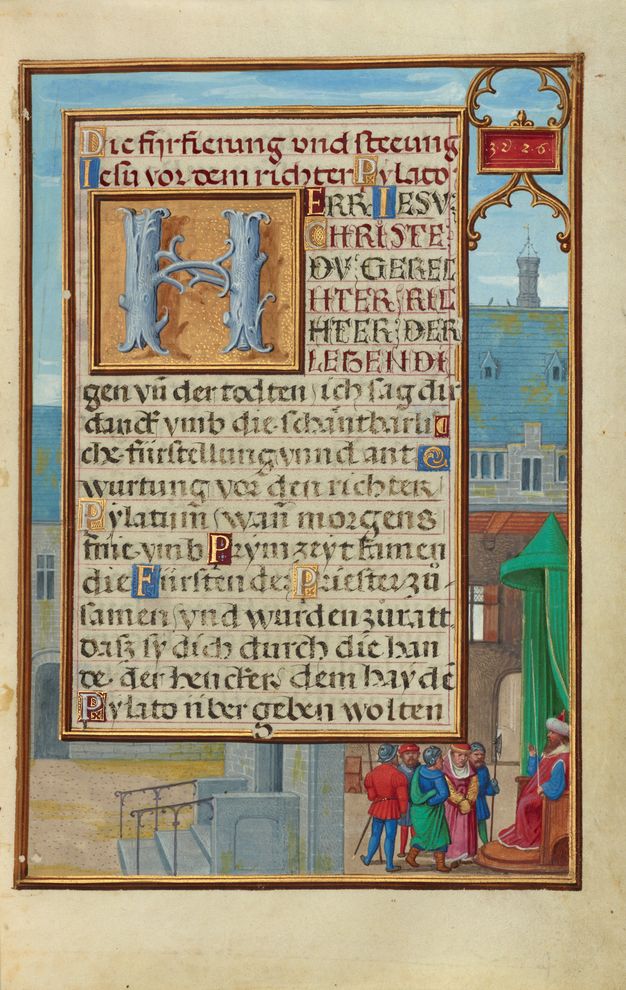

Sometimes works are known by the name of a current or previous

owner, such as the

Prayerbook of Cardinal Albrecht of Brandenburg [ Figure 7a

Figure 7a

Christ before Pilate, about 1525-1530;

artist: Simon Bening (Flemish

illuminator, ca. 1483 - 1561);

tempera colors, gold

paint, and gold leaf, Leaf: 16.8 × 11.4 cm (6 5/8 × 4 1/2

in.);

J. Paul Getty Museum (Los Angeles, CA), Ms.

Ludwig IX 19, fol. 138, 83.ML.115.138v.] [ Figure 7b

Figure 7b

Border with a Captured Prophet before a Prince or

King, about 1525-1530;

artist: Simon Bening (Flemish

illuminator, ca. 1483-1561);

tempera colors, gold

paint, and gold leaf, Leaf: 16.8 × 11.4 cm (6 5/8 × 4 1/2

in.);

J. Paul Getty Museum (Los Angeles, CA), Ms.

Ludwig IX 19, fol. 139, 83.ML.115.139.] or the Lansdowne Herakles [ Figure 5

Figure 5

Lansdowne Herakles, ca. 125 CE;

artist: unknown Roman, after lost

Greek original from School of Polykleitos;

Pentelic

marble, 193.5 cm (height);

J. Paul Getty Museum (Los

Angeles, California), 70.AA.109], which was in the collection of the Marquess of Lansdowne

until 1951.

RELATED CATEGORIES and ACCESS

Information in this category should be repeated in other pertinent subcategories in the following instances. Record the current repository of a work in . Information about the commission of a work of art should be included in the category. Significant events or places associated with the work after its creation should be noted in or . Surrogate images or reproductions available from the present owner of a work should be included in . The place where a work was excavated, and other information about the archaeological site where it was discovered, should be noted in . If the owner of the work is also the sitter in a portrait, record him or her in .

Collectors’ marks or labels may be described and transcribed in , and the presence and significance of these marks should be described here in . Alternate attributions should be included in the category . The association of an attribution to a particular owner should be noted in and discussed in the subcategory. The place where a work was manufactured or made should be specified in .

It should be possible, for example, to locate all the works in a particular collection, or to answer questions such as “What works, now in American collections, were owned by the eighteenth-century Venetian collector Padre Resta?” It may also be useful to identify all works that are or were in a particular place. Varying levels of specificity should be supported either by the use of a hierarchical thesaurus or by including broader geographical entities. Queries may be qualified by date, in order to identify, for example, all works in London between 1700 and 1780 depicting a particular iconographical subject. A scholar interested in the commerce of art may wish to have access to ownership information by the type of transaction (e.g., a bequest or a gift). A study of the critical reception and history of a work, artist, or movement might be enhanced by a comparison of prices or values overtime.

23.1 Provenance Description

DEFINITION

The prose description of the provenance or ownership history of a work of art or architecture, or a group of works.

EXAMPLES

-

before 1835, Sant’Agostino (San Gimignano, Italy);

before 1846, Cardinal Fesch [1763-1839] collection (Rome, Italy).

then to Campana collection;

1863-present, Musée du Louvre (Paris, France)3 -

prior to late 1920s, Kung family (Peking, China).

late 1920s, Peking Palace Museum.

early 1930s, Sir Percival David [1892-1964] collection (London, England).

1977-present, Metropolitan Museum (New York, New York, USA)4 -

1426-late 16th century, commissioned from the artist by Ser Giuliano di Colino di Pietro degli Scarsi di San Giusto, (Santa Maria del Carmine, Pisa, Italy).

by 1892, Adolph Bayersdorfer [1842-1901](Munich, Germany);

possibly 1892-1933, sold to Count Karol Lanckoronski [1848-1933](Vienna, Austria);

1933-1939, by inheritance to his daughter, Karolina Lanckoronski [1898-2002](Vienna, Austria), another daughter, and a stepson ;

1939-1945, looted by the Nazis, in the possession of the Nazis (Schloss Stiesberg, near Wiener-Neustadt, Austria);

1945-1979, restituted to Karolina Lanckoronski [1898-2002](Zürich, Switzerland) and two other Lanckoronski children;

1979, Karolina Lanckoronski through (Heim Gallery, London, England);

1979-present, sold to the J. Paul Getty Museum (Los Angeles, California, USA)5

DISCUSSION and GUIDELINES

Optional: Record the work’s successive owners (or those who had possession of the work), from the first owner to the present owner, if known. The names of ancillary individuals or firms (e.g., agents, dealers, auction houses, consignees) which, while not technically owners, played a role in the transfer of the object from one owner to another, may also be included. Include notes describing the relationship of one owner to another if this elucidates the chain of ownership. Indicate if information about a work’s provenance or ownership is speculative or uncertain.

Form and syntax 6

List the owners in chronological order, from the earliest known owner until the present. Include the following information if known for each owner/agent: the dates of their ownership; the names of the owners; the place where the object was located; and the means by which the work passed from one owner to another. Include the life dates of the owners, if known, in brackets. Enclose the names of dealers, auction houses, or agents in parentheses to distinguish them from private owners.

Note lacunae in the provenance. Use a semicolon to indicate that the work passed directly between two owners (including dealers, auction houses, or agents); use a period to separate two owners (including dealers auction houses or agents) if a direct transfer did not occur or is not known to have occurred. Indicate uncertain information with possibly, probably, or a question mark. Indicate methods of transfer with sold, by descent, by inheritance, given, and other terms as necessary. Use the subcategory to document or clarify information, including any lacunae in the known chain of ownership. Use to cite published or unpublished sources for the information.

Information may be extrapolated from other evidence, rather than specifically derived from source documents. This is often the case with works that have been lost, stolen, or destroyed. A clear indication of the degree of certainty and the basis for the information recorded in this subcategory is essential.

TERMINOLOGY/FORMAT

Free-text: This is not a controlled field. If retrieval is required on provenance information, index this information in the pertinent controlled subcategories elsewhere in the record.

RELATED CATEGORIES and ACCESS

Index information about the provenance in the other subcategories. It is highly recommended to record the sources of the information in the . Transcribe source information as necessary in ; this is particularly important for unpublished sources, such as inventories and letters.

23.1.1 Acquisition Description

DEFINITION

The prose description of the most recent owner or location of the work, prior to acquisition by the current owner or repository.

EXAMPLE

- Collection of Mr. and Mrs. Paul Mellon

DISCUSSION and GUIDELINES

Optional: Record the last owner or location of the work. This would be the most recent entry in the subcategory. It may also be repeated in .

TERMINOLOGY/FORMAT

Free-text: This is not a controlled field. If retrieval is required on information in this field, index the information in the pertinent controlled subcategories elsewhere in the record.

23.2 Transfer Mode/Method of Acquisition

DEFINITION

The means by which a work entered the collection of a particular individual or corporate body.

EXAMPLES

- commission

- gift

- donation

- bequest

- endowment

- purchase

- auction

- exchange

- transfer

- loan

- rental

- consignment

- collection of artist

- original owner

- field collected

- lost

- destroyed

- stolen

- confiscated

- looted

- unknown

DISCUSSION and GUIDELINES

Optional: Record a term or terms describing the method of transfer from one owner to another. Use lower case.

Since the ownership of a work can be transferred in many different ways, it is important to record how a certain individual or corporation came into possession of a work. It should also be indicated here if a work has been lost, stolen, or destroyed. Categorizing the method of transfer makes it possible to distinguish between varying types of acquisitions, thus enhancing the study of the history of collecting. It may be possible to establish the acquisition method definitively, based on a published document, such as a sale catalog. Published and unpublished documents, including sales catalogs, bills of sale, wills, and letters, may provide information about the transfer of a work. The means by which a work passed from one person to another may have to be extrapolated from other information about ownership, or may not be known.

TERMINOLOGY/FORMAT

Controlled list: Control this subcategory with a controlled list derived from terms listed in the “Examples” section above, and other terms as necessary. Use the Art & Architecture Thesaurus (AAT) Hierarchy Display (especially the Events, Functions, and Physical Activities hierarchies) to find additional terminology.

23.3 Cost or Value

DEFINITION

The monetary value of a work in a specific currency at the time of ownership transfer. This can be either a purchase price or an evaluation.

EXAMPLES

- around $500,000 US

- documented as £1500

- probably 50-55 gold florins

DISCUSSION and GUIDELINES

Optional Record the fee or other compensation paid when the work was transferred from one owner to the other. Include the amount, the currency, the type of transaction, and the type of payment, if applicable. Since historical currencies are difficult to convert into modern ones, it is important to record the value as it is found in documentation; however, a conversion into modern equivalents may also be included. Express uncertainty or ambiguity here; evaluations or estimations may be expressed as a range.

Note that the cost or value is often considered confidential information, especially in relation to a contemporary acquisition by a museum, gallery, or private collector.

TERMINOLOGY/FORMAT

Free text: This is not a controlled field. Even though this is a free-text field, the use of consistent format and controlled terminology is recommended for clarity.

23.3.1 Valuation

DEFINITION

An expression of the value for display.

EXAMPLES

- 1000 Belgian Francs

- £1500

- 48,000 yen

DISCUSSION and GUIDELINES

Optional: Record a display form for the value of the work, including currency and amount when the work was transferred from one owner to another.

TERMINOLOGY/FORMAT

Free text: This is not a controlled field.

23.3.1.1 Valuation Amount

DEFINITION

The numerical expression of the value, as expressed in the display Valuation(23.3.1) subcategory.

EXAMPLES

- 1000

- 110,000

- 48,000

DISCUSSION and GUIDELINES

Optional: Record whole numbers or decimal fractions recorded in the subcategory.

TERMINOLOGY/FORMAT

Controlled format: Use whole numbers or decimal fractions only.

23.3.1.2 Currency Unit

DEFINITION

The type of currency recorded in the Valuation(23.3.1) subcategory.

EXAMPLES

- United States dollar

- Florentine florin

- South Korean won

DISCUSSION and GUIDELINES

Optional: Record the type of currency recorded in .

TERMINOLOGY/FORMAT

Controlled list: Use abbreviations or terms consistently. Use an authority, such as the Art & Architecture Thesaurus (AAT) Hierarchy Display; use the narrower context terms for AAT 300411993 currencies (systems of money). Abbreviations may be used (e.g., FRF rather than French franc); however, note that if historical currencies are included in the data base, there may not be standard abbreviations.

23.4 Legal Status

DEFINITION

The legal status of the work.

EXAMPLES

- public property

- scheduled property

- registered property

- national treasure

DISCUSSION and GUIDELINES

Optional: Record the legal status of the work or art or architecture.7 Note that the legal status of a work may change over time. Use lower case terminology, unless the term includes a proper name.

TERMINOLOGY/FORMAT

Controlled list: Control this subcategory with a controlled list derived from terms in the “Examples” section above, and other terms as necessary.

23.5 Owner/Agent

DEFINITION

The name of an individual or corporate body (institution, agency, or group) that owned or was in posession of the work of art or architecture, or served as an agent or intermediary in its transfer from one owner to another.

EXAMPLES

- Mellon, Paul

- Contini-Bonacossi, Alessandro, Count

- Bing, S.

- Catherine II of Russia

- Thomas, 2nd Earl of Arundel

- National Gallery of Art (Washington, DC)

- Santa Maria Novella (Florence, Italy)

- M. Knoedler & Co.

- Christie, Manson and Woods, Ltd.

- Sueca Family

- private collection

- unknown

DISCUSSION and GUIDELINES

Optional: Record the name of the individual, group, or corporate body that owned or had possession of the work/object during the specified period of time.

Form and syntax

Ideally, this should be a link to the , where a full record containing the owner’s variant names and biographical information will be stored and available for retrieval. See the for guidelines in constructing personal names.

Usually this subcategory will contain a personal or corporate name. If a work had multiple owners during one period of ownership, there may be multiple owners indexed for this period. This situation may occur with married couples or with other individuals or corporations that hold joint ownership of an object or group of objects. For example, the Third Duke of Bridgewater, the Fifth Earl of Carlisle, and the Second Earl of Gower together purchased pictures from the Orléans Collection from the dealer Michael Bryan in London in 1798.

Indicate an anonymous private collection by using the term private collection. Express uncertainty and nuance regarding the owner in the subcategory. Use the term unknown to indicate periods when the owner or whereabouts of the work was unknown.

TERMINOLOGY/FORMAT

Authority: Control this subcategory with the , which can be populated from the controlled vocabularies named below. An authority with hierarchical structure, cross referencing, and synonymous names is recommended.

Published sources of vocabulary and biographical information include the following: LC Name Authorities, United List of Artist Names (ULAN), Canadiana Authorities, and Yale British Artists. Consult AACR for general guidelines regarding the formatting of names.

23.5.1 Owner/Agent Role

DEFINITION

The role played by an individual or corporate body with regard to an object/work’s ownership, posession, or transfer of ownership.

EXAMPLE

- owner

- dealer

- auction house

- agent

- occupant

DISCUSSION and GUIDELINES

Optional: Record the owner’s or other agent’s role in relation to a particular transaction in the transfer of the work. Use lower case.

Specifying roles makes it possible to distinguish between owners (who hold legal title to the work), agents or auction houses (which do not hold legal title to the work), and dealers or commercial galleries (which may or may not hold title, but which own the work for commercial purposes). The role of an owner or agent in a work’s provenance is seldom cited explicitly in documents, but can often be discerned from biographical or historical sources.

TERMINOLOGY/FORMAT

Controlled list: Control this subcategory with a controlled list: owner, dealer, auction house, agent, and other terms as necessary. Use the Art & Architecture Thesaurus (AAT) Hierarchy Display(especially Agents facet), the Dictionarium Museologicum, and other published sources.

RELATED CATEGORIES and ACCESS

Record the person’s or corporate body’s life roles (e.g., businessman, count, museum) in the .

23.6 Ownership Place

DEFINITION

The place where the work was housed while in the possession of a particular owner.

EXAMPLES

- Amsterdam (Netherlands)

- Palm Beach (Florida, United States)

- 5 Cheyne Walk, Chelsea (London, England, United Kingdom)

- Boadilla del Monte (Spain)

- Badger Hall (Shropshire, England, United Kingdom)

- Washington (DC, United States)

- Styria Studios (Glendale, California, United States)

DISCUSSION and GUIDELINES

Optional: Record the name of the place of ownership. The location may be unknown or uncertain; it may be known at various levels of specificity. If an explanation regarding the place of ownership is necessary (e.g., using the terms probably or possibly), explain it in the subcategory.

Form and syntax

For guidelines regarding the syntax and format of place names, see and the .

Note that an individual owner may have more than one residence, and corporations may also have many places of business. In such cases, record either the owner’s principal residence or a corporation’s head office or index all possible locations where the work may have been located while under the care of this owner. For an auction house, gallery, or dealer, note the location of the branch that made the sale.

While it is not always possible to establish specifically where a work was held, location should be recorded as precisely as possible. Places could be identified as specifically as the name of a particular building or street address, such as Buckingham Palace (London, England, United Kingdom) or Monticello (Albemarle county, Virginia, USA). It is also possible that scholarship can only place a work in a particular country or area, without a more precise location being known.

TERMINOLOGY/FORMAT

Authority: Control this subcategory with the , which can be populated with terminology from the TGN, NGA (NIMA) and USGS, Canadiana Authorities, LC Name Authorities, and LCSH.

23.7 Ownership Date

DEFINITION

The period of time during which the work belonged to or was in the possession of a particular owner or agent.

EXAMPLES

- 1940-1949

- by 1848-ca. 1880

- 17 June 1955 - November or December 1956

- 26 May 1991

- after 1640

- from 1348

- 14th-18th centuries

DISCUSSION and GUIDELINES

Optional: Record a year, a span of years, or a phrase that describes the specific or approximate date associated with the ownership or possession of the work. Include nuance and expressions of uncertainty, as necessary.

Form and syntax

Follow rules for display dates as recorded in .

The date of a particular ownership may be unknown or known only as an approximate date within a span. In some instances, both the date of acquisition and the date of disposition will be documented. In other cases, only dates such as the owner’s life dates may be known. A publication or document may place a work in an owner’s possession by a certain date, without specifying when it entered that collection. A clear distinction must be made between firmly documented dates and those established or extrapolated by reference to other parameters, such as the owner’s life dates, the dates of ownership of the previous owner, or the dates of an exhibition or publication in which a named individual is listed as owner.

For lost or stolen works, the date of the disappearance should be indicated. For works that have been destroyed, the date of their destruction should be specified.

TERMINOLOGY/FORMAT

Free-text: This is not a controlled field. Maintain consistent capitalization, punctuation, and syntax where possible. Index the dates in the controlled and subcategories.

23.7.1 Earliest Date

DEFINITION

The earliest possible date when t he work belonged to or was in the possession of a particular owner or agent.

EXAMPLES

- 1940

- 1848

- 1971-12-23

DISCUSSION and GUIDELINES

Optional: Record the earliest year when a particular owner or agent had control of the work, as indicated in the subcategory.

Form and syntax

Always record years in the proleptic Gregorian calendar in the indexing dates fields. Record the precise day and time, if possible. Use the following syntax: YYYY-MM-DD (year, month, day, separated by dashes), if possible. The standards suggest alternate possibilities; you may use an alternative syntax if you are consistent and it is compliant with the standards. It is optional to record ; however, if you record a value here, you must also record . For additional rules, see .

TERMINOLOGY/FORMAT

Controlled format: Date information must be formatted consistently to allow retrieval. Local rules should be in place. Suggested formats are available in the ISO Standard and W3 XML Schema Part 2.

-

ISO 8601:2004 Representation of dates and times. International Organization for Standardization. Data Elements and Interchange Formats. Information Interchange. Representation of Dates and Times. Geneva, Switzerland: International Organization for Standardization, 2004.

23.7.2 Latest Date

DEFINITION

The latest possible date when the work belonged to or was in the possession of a particular owner or agent.

EXAMPLES

- 1949

- 1885

- 1971-12-23

DISCUSSION and GUIDELINES

Optional: Record the latest year when a particular owner or agent had control of the work, as indicated in the subcategory.

Form and syntax

Always record years in the proleptic Gregorian calendar in the indexing dates fields. Record the precise day and time, if possible. Use the following syntax: YYYY-MM-DD (year, month, day, separated by dashes), if possible. The standards suggest alternate possibilities; you may use an alternative syntax if you are consistent and it is compliant with the standards. It is optional to record ; however, if you record a value here, you must also record . For additional rules, see .

TERMINOLOGY/FORMAT

Controlled format: Date information must be formatted consistently to allow retrieval. Local rules should be in place. Suggested formats are available in the ISO Standard and W3 XML Schema Part 2.

-

ISO 8601:2004 Representation of dates and times. International Organization for Standardization. Data Elements and Interchange Formats. Information Interchange. Representation of Dates and Times. Geneva, Switzerland: International Organization for Standardization, 2004.

23.8 Owner’s Number

DEFINITION

Any numbers assigned to a work by a specific owner or agent in its transfer of ownership.

EXAMPLES

- DR 1989:0001

- JP49739

- 1988.00017.0013

- NK 12/62

- q60

- Pall. XXIII, fol.1

- 83.AE.362

- plate 12

- item 134

DISCUSSION and GUIDELINES

Optional: Record the object identification number used by a specific owner or agent during transfer. Numbers may have prefixes or suffixes that are vital to their meaning.

Identification numbers are frequently affixed to or inscribed directly on the object. They also appear in museum catalogs, owners’ lists, inventories, and other primary sources. Occasionally, identification numbers can be found in secondary literature, such as exhibition catalogs and catalogues raisonnés.

Identification numbers are often accession numbers, assigned by museums and composed of multiple parts (e.g., PA-1987.56.98.1). These can include the year of acquisition; the number of the acquisition within that year; and the number of the item within that acquisition. Ideally, there is no duplication in accession numbers within a single museum; however, this is not always the case, especially in older collections. A single object may have multiple accession numbers (for example, when fragments of an object are acquired at different times).

TERMINOLOGY/FORMAT

Free text: The format of the number will vary depending on its type and source. Types of numbers or the roles numbers play may in some cases be described with terms from a controlled vocabulary such as the Dictionarium Museologicum.

23.8.1 Number Type

DEFINITION

The type of number assigned to a work by a specific owner or agent in its transfer of ownership.

EXAMPLES

- accession number

- collection number

- registration number

- location symbol

- collector’s number

- identification number

- object identification

DISCUSSION and GUIDELINES

Optional: Record a term describing the type of number, if known. Use lower case.

TERMINOLOGY/FORMAT

Controlled list : Control this subcategory with a controlled list, using the terms in the “Examples” section above, and others as necessary.

23.8 Owner’s Credit Line

DEFINITION

A formal public statement about the ownership, transfer of ownership, acquisition, source, or sponsorship of a work’s acquisition, suitable for use in a display label or publication.

EXAMPLES

- Rogers Fund, 1919 (19.164)

- Purchase, William H. Riggs Gift and Rogers Fund, 1919 (19.131.1, 2)

- Gift of J. Pierpont Morgan, 1917 (17.190.173a, b)

- Gift of the Robert Lehman Foundation, Inc. 484.1976.4

- Gift of the Collectors Committee

- Samuel H. Kress Collection

- Given in Loving Memory of Gert Smithrion

- Bequest of James W. Toolhand

- U.S. Army Corps Collection

DISCUSSION and GUIDELINES

Optional: Record the owner’s formal statement indicating how the work came into the collection. Include information such as an acknowledgment of the acquisition fund, or the name of the specific collection to which a work belongs within a larger museum context.

Form and syntax

Capitalize proper names. Otherwise, record the statement verbatim.

This subcategory provides an approved text that can be used when publishing a work, or included on an exhibition label. In general, the credit line cites the name of a benefactor who assisted with the acquisition of the work. The text of the credit line is often written in consultation with the benefactor. The credit line is often displayed with basic tombstone information about the work (e.g., artist name, title of the work, creation date, media, measurements, name of repository); the accession number; and a copyright statement.

TERMINOLOGY/FORMAT

Free text: This is not a controlled field. Transcribe the credit line verbatim as expressed by the owner.

23.10 Remarks

DEFINITION

Additional notes or comments pertinent to information in this category.

DISCUSSION and GUIDELINES

Optional: Record a note containing additional information related to this category. Use consistent syntax and format. For rules regarding writing notes, see .

FORMAT/TERMINOLOGY

Free-text: This is not a controlled field. Use consistent syntax and format.

23.11 Citations

DEFINITION

A reference to a bibliographic source, unpublished document, or individual opinion that provides the basis for the information recorded in this category.

DISCUSSION and GUIDELINES

Optional: Record the source used for information in this category. For a full set of rules for citations, see .

TERMINOLOGY/FORMAT

Authority: Ideally, this information is controlled by citations in the citations authority; see .

23.11.1 Page

DEFINITION

Page number, volume, date accessed for Web sites, and any other information indicating where in the source the information was found.

DISCUSSION and GUIDELINES

Optional: For a full set of rules for pages, see .

TERMINOLOGY/FORMAT

Free-text: This is not a controlled field. Use consistent syntax and format.

Examples

Example of a relatively short provenance statement:

-

Ownership/Collecting History:

descended through eight generations in the family of John Tufts [1754-1839] (Sherborn, Massachusetts, USA).

by 1921, Wallace Nutting [1861-1941] (Framingham, Massachusetts, USA);

1921-1951, Mrs. J. Insley Blair [died 1951] (Tuxedo Park, New York, USA);

1951-present, Metropolitan Museum of Art (New York, New York, USA).8

Example of a longer provenance statement:

-

Ownership/Collecting History:

from 1783, commissioned by the Infante Don Luis de Borbón [1727-1785] (Palace of Arenas de San Pedro, near Avila, Spain);

from 1785, by inheritance to his daughter, the sitter María Teresa de Borbón [1779-1828] (Palace at Boadilla del Monte, near Madrid);

from 1828, by inheritance to her only child, Carlota Luisa de Godoy y Borbón [1800-1886], Condesa de Chinchón, Duquesa de Alcudia y de Sueca, Boadilla del Monte, in whose possession it was recorded in 1867 and 1886;

from 1886, by inheritance to her son, Adolfo Ruspoli [1822-1914], Duque de Sueca, Conde de Chinchón;

1914, possibly purchased by the family at his (liquidation sale, Paris, 7 February 1914);

his daughter, Maria Teresa Ruspoli y Alvarez de Toledo, wife of Henri-Melchior Cognet Chappuis, Comte de Maubou de la Roue (Paris, France);

by 1951, her nephew, Don Camilo Carlos Adolfo Ruspoli y Caro [1904-1975], Conde de Chinchón, Duque de Alcudia y de Sueca (Madrid, Spain).

by March 1957, sold by the family, (Wildenstein & Co., New York, New York, USA);

2 March 1959, purchased by Ailsa Mellon Bruce (New York, New York, USA);

1970-present, gift to National Gallery of Art (Washington, DC, USA) 9

Example where indications of uncertainty are used, e.g., possibly, probably, question mark:

-

Ownership/Collecting History:

before 1648-?, possibly Monseigneur de Housset, French ambassador to Venice (France; Italy).

to 1777, probably Pierre Louis Paul Randon de Boisset, [died 1776] (Paris, France).

1777, Chariot.

1777-?, Lebrun.

probably after 1860, Sir Francis Cook, 1st Baronet [1817-1901] (England).

by 1903-1920, Sir Frederick Lucas Cook, 2nd Baronet [died 1920] (England).

1920-still in 1932, by inheritance to Sir Herbert Frederick Cook, 3rd Baronet[died 1939] (England).

to 1948, Count Alessandro Contini-Bonacossi [died 1951] (Florence, Italy);

1948-1961, Samuel H. Kress Foundation (New York, New York, USA);

1961-present, accessioned 09 December 1961 by Seattle Art Museum (Seattle, Washington, USA) 10

Example with a citation for an unpublished source included:

-

Ownership/Collecting History:

before 1927, Frits Lugt [1884-1970] (Amsterdam, Netherlands).

1927, with (Van Diemen, Berlin, Germany). Private collection (southern Germany).

1930, with (Vitale and Bloch, Berlin). 1932, Dresden Gallery, 1932.

ca. 1935, Frits Haussmann (Berlin, Germany).

1948-1949, with (Jacob M. Heimann, New York, New York, USA);

1949-present, purchased 1949 by Anne R. and Amy Putnam for the Fine Art Society (now San Diego Museum of Art) (San Diego, California, USA)

Citation: SDMA curatorial files, Jacob M. Heimann correspondence to Reginald Poland, April 8, 1948.11

Example with a notation of the price paid, e.g., ducats and franks:

-

Ownership/Collecting History:

1838, painted in 1838 for Mathias Feldmüller the Younger), wood merchant (Vienna, Austria) for 80 ducats.

from ca. 1852, sold ca. 1852 to Jakob Fellner (Vienna, Austria); 1871, (his collection sale, Vienna, P. Kaeser, 14-15 December 1871 (lot 9));

from 1871, sold 1871 for ƒ800 to Löscher, a Viennese dealer.

by 1927, Baron Franz Wertheimer (Vienna, Austria); His heirs, United States.

1991, bought by (Galerie Sanct Lucas, Vienna, Austria);

1991-present, purchased 1991 by the Cleveland Museum of Art (Cleveland, Ohio, USA)

Citation: According to annotated sales catalogue in the Netherlands Institute for Art History, The Hague.12

Example for architecture, without a free-text statement:

-

Owner/Agent: Martin, Darwin D.

Role: owner

Owner/Agent: Martin, Isabelle Role: occupant

Owner/Agent: Martin House Restoration Corporation Role: owner

Example for architecture, including status as national treasure:

-

Owner/Agent: Akamatsu Sadanori

Role: owner

Date: from 1346 Earliest: 1346 Latest: 1400

Owner/Agent: Hideyoshi Role: owner

Date: after 1577 Earliest: 1577 Latest: 1601

Owner/Agent: Ikeda Terumasa Role: owner

Date: 1601-1613 Earliest: 1601 Latest: 1613

Owner/Agent: Ministry of Culture (Japan) Role: owner

Date: since 1931 Earliest: 1931 Latest: 9999

Legal Status: national treasure

Example for a painting, with free-text provenance statement and associated indexing fields:

-

Ownership/Collecting History:

1924, sold 21 October 1924 by the artist to (Galerie Bernheim-Jeune, Paris, France);

from 1924, sold 24 October 1924 to Georges Bernheim (Paris, France);

sold to Paul Rosenberg (Paris, France);

sold to (Pierre Matisse Gallery, New York, New York, USA);

1951, sold 1951 to (Paul Rosenberg and Co., New York, New York, USA);

Alexandre Rosenberg (New York, New York, USA);

ca.1977, sold to (Eugene Victor Thaw and Co., New York, New York, USA);

1978-1985, sold January 1978 to Mr. and Mrs. Paul Mellon (Upperville, Virginia, USA);

1985-present, gift 1985 to National Gallery of Art (Washington, DC, USA).

1. Date: 1924 Earliest: 1924 Latest: 1924 Transfer Mode: collection of artist Owner/Agent: Matisse, Henri Role: artist Place: Paris (France)

2. Date: 21 October 1924 Earliest: 1924-10-21 Latest: 1924-10-21 Transfer Mode: purchase Owner/Agent: Galerie Bernheim-Jeune Role: dealer Place: Paris (France)

3. Date: from 24 October 1924 Earliest: 1924-10-24 Latest: 1924-10-24 Transfer Mode: purchase Owner/Agent: Bernheim, Georges Role: owner Place: Paris (France)

4. Transfer Mode: purchase Owner/Agent: Rosenberg, Paul Role: owner Place: Paris (France)

5. Transfer Mode: purchase Owner/Agent: Pierre Matisse Gallery Role: dealer Place: New York (New York, USA)

6. Date: 1951 Earliest: 1951 Latest: 1951 Transfer Mode: purchase Owner/Agent: Paul Rosenberg and Co. Role: dealer Place: New York (New York, USA)

7. Date: ca. 1977 Earliest: 1975 Latest: 1979 Transfer Mode: purchase Owner/Agent: Eugene Victor Thaw and Co. Role: dealer Place: New York (New York, USA)

8. Date: January 1978-1985 Earliest: 1978 Latest: 1985 Transfer Mode: purchase Owner/Agent: Mellon, Paul Role: owner Owner/Agent: Mellon, Paul, Mrs. Role: owner Place: Upperville (Virginia, USA)

9. Date: 1985-present Earliest: 1985 Latest: 9999 Transfer Mode: gifted Owner/Agent: National Gallery of Art Role: owner Place: Washington, (DC, USA) 13

Revised 21 February 2024

by Emily Benoff

Notes

-

See Yeide, Nancy H., Konstantin Akinsha, and Amy L. Walsh. AAM Guide to Provenance Research. Washington, DC: American Association of Museums, 2001. A bibliography of online databases and other sources may be found on the Web site of the Seattle Art Museum at https://www.seattleartmuseum.org/art-and-artists/rights-and-resources. ↩︎

-

Research projects, such as the J. Paul Getty Trust’s Provenance Index, https://piprod.getty.edu/starweb/pi/servlet.starweb?path=pi/pi.web, document the provenance of a wide range of works. ↩︎

-

From Patricia Harpring. Sienese Trecento Painter Bartolo di Fredi. London and Toronto: Associated University Presses, 1993, 156; for Bartolo di Fredi, Purification of the Virgin, tempera on panel, ca. 1390-1409. ↩︎

-

Information (but not necessarily the format) is from the Metropolitan Museum of Art, http://www.metmuseum.org. For Night-Shining White, Tang dynasty (618-907), 8th century. Attributed to Han Gan (Chinese, act. 742-756). China. Handscroll; ink on paper; 12 1/8 x 13 3/8 in. (30.8 x 34 cm). Purchase, The Dillon Fund Gift, 1977 (1977.78). ↩︎

-

Information (but not necessarily the format) is from the J. Paul Getty Museum, www.getty.edu. For Saint Andrew. Masaccio (Tommaso di Giovanni Guidi) (Italian (Florentine), 1401-1428). 1426. Tempera and gold leaf on panel. Unframed [panel]: 52.4 x 32.1 cm (20 5/8 x 12 5/8 in.) Surviving original painted surface: 44.9 x 30.2 cm (17 11/16 x 11 7/8 in.) framed: 69.2 x 37.8 x 5.1 cm (27 1/4 x 14 7/8 x 2 in.). 79.PB.61. ↩︎

-

Guidelines are informed by the suggestions in the AAM Guide to Provenance Research, cited above. ↩︎

-

See Robin Thornes, Protecting Cultural Objects Through International Documentation Standards: A Preliminary Survey. Santa Monica, California: J. Paul Getty Trust, 1995. ↩︎

-

Information (but not necessarily the format) is from the Metropolitan Museum of Art, http://www.metmuseum.org. For unknown artist, Turned Armchair, 1640-1680. Made in New England, Eastern Massachusetts, America. Ash; 44 3/4 x 23 1/2 x 15 3/4 in. (113.7 x 59.7 x 40.0 cm). Bequest of Mrs. J. Insley Blair, 1951 (51.12.2). ↩︎

-

Information (but not necessarily the format) is from the National Gallery of Art, http://www.nga.gov. For Francisco de Goya (Spanish, 1746-1828); María Teresa de Borbón y Vallabriga, later Condesa de Chinchón, 1783; oil on canvas, 134.5 x 117.5 cm (53 x 46 1/4 in.); Ailsa Mellon Bruce Collection; 1970.17.123. ↩︎

-

Information (but not necessarily the format) is from the Seattle Art Museum, http://www.seattleartmuseum.org/. For workshop of Paolo di Gabriele di Piero Caliari (known as Veronese) (Italian, 1528-1588); Venus and Adonis; before 1580; oil on canvas; 88 3/8 x 66 1/4 in. (224.4 x 168.3 cm); Gift of the Samuel H. Kress Foundation, 61.174. ↩︎

-

Information (but not necessarily the format) is from the San Diego Museum of Art, http://www.sdmart.org/. For Bernardo Bellotto (Italian (Venetian), 1721-1780); Architectural Capriccio with a Baroque Palace Beside a Moat; ca. 1765; oil on canvas; 19 x 31 3/8 in. (48.3 x 79.7 cm); Gift of Anne R. and Amy Putnam, 1949:68. ↩︎

-

Information (but not necessarily the format) is from the Cleveland Museum of Art, http://www.clevelandart.org/. For Friedrich Amerling (Austrian, 1803 - 1887); The Young Eastern Woman (Die junge Morgenländerin); 1838; oil on fabric; framed: 106.5cm x 90.5cm x 9.cm, unframed: 88.5cm x 71.5cm; 1991.163; Mr. and Mrs. William H. Marlatt Fund. ↩︎

-

Information (but not necessarily the format) is from the National Gallery of Art, http://www.nga.gov. For Henri Matisse (French, 1869-1954); Pianist and Checker Players, 1924; oil on canvas, 73.7 x 92.4 cm (29 x 36 3/8 in.); Collection of Mr. and Mrs. Paul Mellon; 1985.64.25. ↩︎